Navigating the 2026 EMI Licensing in Cyprus Landscape: From EMD2 to the Unified PSD3 Framework

The Electronic Money Institution (EMI) sector in Cyprus is undergoing its most significant shift in a decade. With the Payment Services Directive 3 (PSD3) and the Payment Services Regulation (PSR), the EU is merging the PI and EMI regimes into a single, harmonized framework.

At CX Financia, we don’t just help you apply for an EMI license; we architect an institution that is “PSD3-Ready” on Day 1, ensuring your business is fully grandfathered into the new 2027 unified regime without costly technical retrofits.

EMI vs. PI: Why Choose the €350,000 Capital Tier?

While the capital requirement for an EMI is higher than a standard Payment Institution, the strategic advantages in 2026 are unparalleled:

Strategic Insight: For firms looking to issue Stablecoins (EMTs) under MiCA, the Cyprus EMI license is the most robust and tax-efficient foundation in the Eurozone.

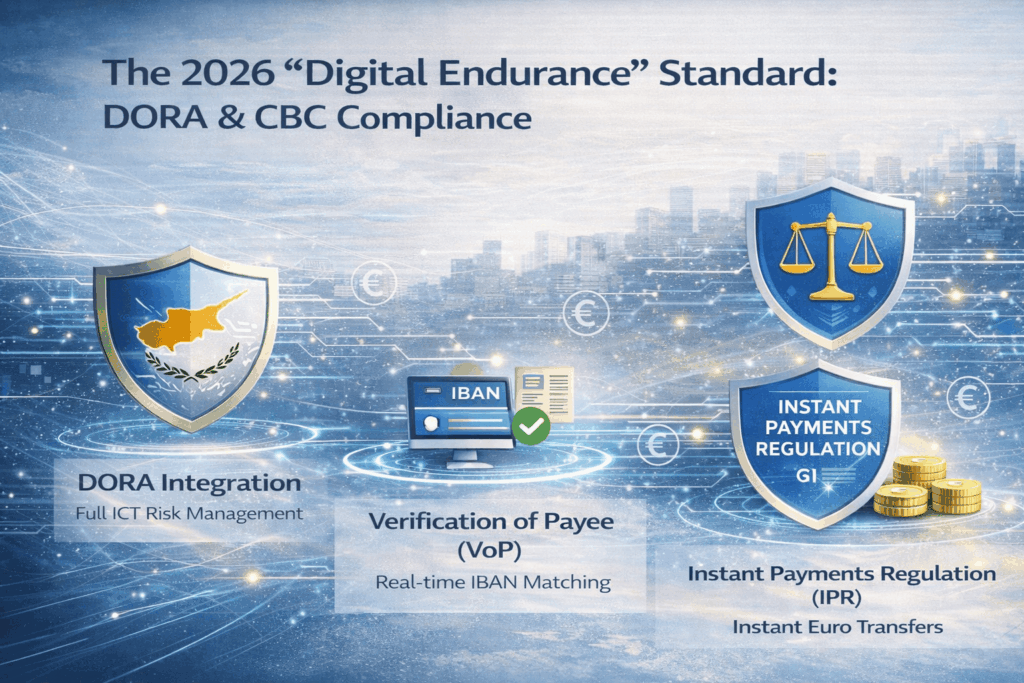

The 2026 “Digital Endurance” Standard: DORA & CBC Compliance

Obtaining an EMI license from the Central Bank of Cyprus (CBC) now requires proving your firm’s digital endurance.

- DORA Integration: Since January 2025, every EMI application must include a full ICT Risk Management framework.

- Verification of Payee (VoP): Your technical program must now support the October 2025 mandate for real-time IBAN-name matching to prevent fraud.

- Instant Payments Regulation (IPR): We help you design your systems to meet the 2026/2027 deadlines for instant credit transfers in Euro.

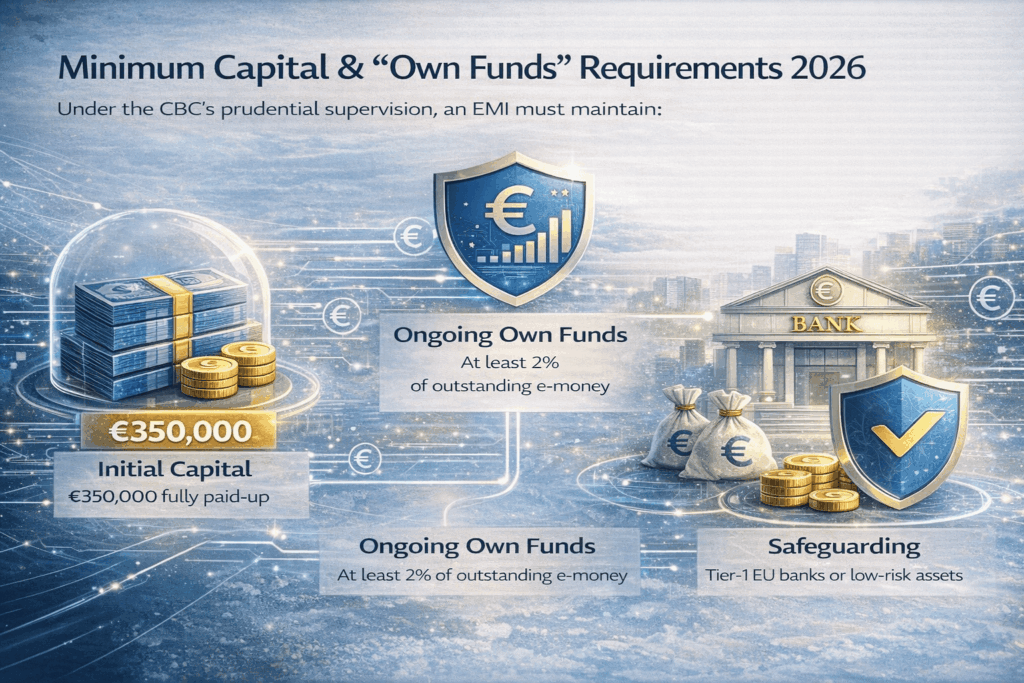

Minimum Capital & “Own Funds” Requirements 2026

Under the CBC’s prudential supervision, an EMI must maintain:

- Initial Capital: €350,000 fully paid-up at the time of authorization.

- Ongoing Own Funds: Equal to at least 2% of the average outstanding e-money issued by the institution.

- Safeguarding: Mandatory “Safeguarding Accounts” with Tier-1 EU banks or specific low-risk investment assets.

The CX Financia EMI Roadmap: Path to EU Passporting

We target a 9-to-12 month activation by utilizing a Pre-Submission Success Filter that clears the “Adequacy Phase” faster.

Phase 1: Substance & Governance Build (Months 1-2)

- Recruitment: Securing the mandatory “4-Eyes” local directors (typically 2 Executive and 3 Non-Executive).

- Manuals: Drafting DORA-compliant Internal Operations Manuals (IOM) and AML/KYC policies tailored for e-money flows.

Phase 2: CBC Submission & Banking Rails (Months 3-9)

- Liaising with the CBC throughout the review.

- Safeguarding Support: Assisting in the opening of safeguarding accounts—the most critical hurdle for any EMI.

Phase 3: Activation & 2027 Grandfathering (Month 10+)

- Final CBC audit and activation.

- EU Passporting: Notifying EEA regulators to allow your firm to issue wallets across 27 member states.

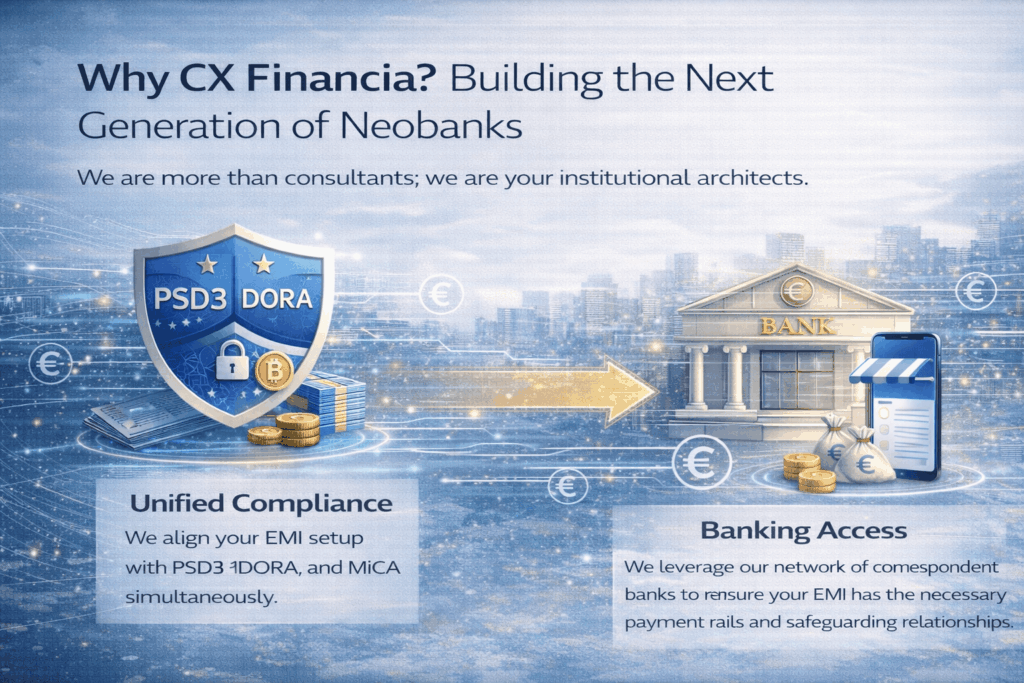

Why CX Financia? Building the Next Generation of Neobanks

We are more than consultants; we are your institutional architects.

- Unified Compliance: We align your EMI setup with PSD3, DORA, and MiCA simultaneously.

- Banking Access: We leverage our network of correspondent banks to ensure your EMI has the necessary payment rails and safeguarding relationships.

Ready to Architect Your Neobank?

Don’t settle for a generic permit. Build a resilient, future-proof Electronic Money Institution with Cyprus’s leading regulatory experts.

FAQ – Cyprus EMI Licensing 2026

What is the "Grandfathering" process for EMIs under PSD3?

Existing EMIs will likely be given a transition period (2026-2027) to adapt to the new unified Payment Institution status. By working with us, your 2026 application will already meet the higher PSR (Payment Services Regulation) standards.

Does an EMI need a MiCA license to issue Stablecoins?

Yes. Under MiCA, an EMI is eligible to issue E-Money Tokens (EMTs), but you must notify the CBC and CySEC and meet specific whitepaper requirements.

How many local staff members are required for a Cyprus EMI?

The CBC expects a “real mind and management” presence. This usually involves 5 Directors and key heads of departments (Compliance, Risk, IT) based in Cyprus.